The landscape of personal finance in India is undergoing a massive shift. While traditional

wealth creation strategies like mutual funds, equities, and real estate continue to dominate

headlines, a critical foundation of financial planning is often overlooked: risk protection.

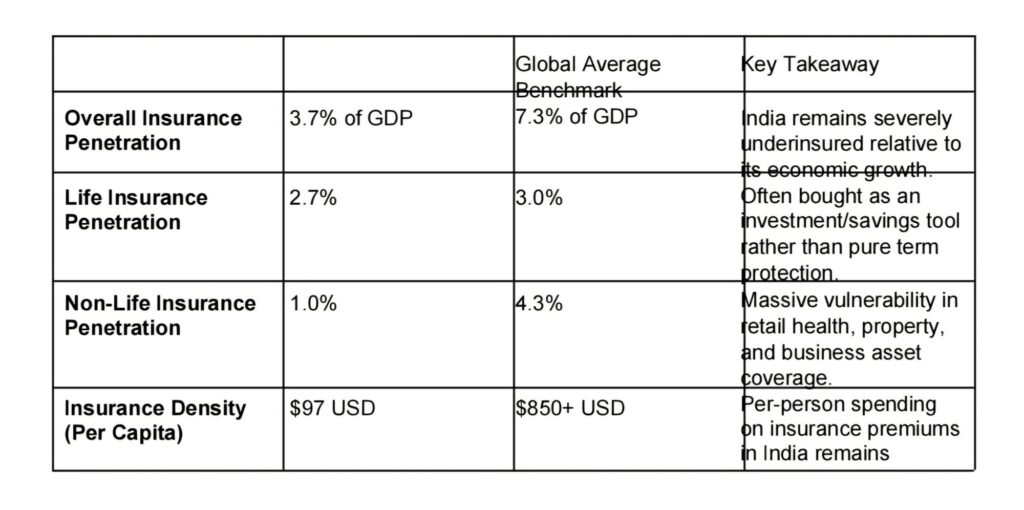

According to data from the Insurance Regulatory and Development Authority of India (IRDAI),

India’s overall insurance penetration stands at just 3.7%—roughly half of the global average

of 7.3%. This massive gap highlights a stark reality: while millions of Indian households are

generating wealth, a singular medical emergency or unforeseen event could easily wipe out

years of savings.

As we look at the economic ecosystem, securing comprehensive insurance is no longer just a

tax-saving checklist item—it is an absolute non-negotiable for robust financial survival.

1. The Real Indian Insurance Deficit (By the Numbers)

To truly understand why protection matters, we must look at the structural gap between life

insurance and non-life insurance (health, motor, home) across the country.

The latest financial data highlights a significant imbalance in how Indians approach risk

coverage:

Insurance Metric (India) Current Status

What is Insurance Penetration vs. Density?

Insurance Penetration: The percentage of a country’s Gross Domestic Product (GDP) written in insurance premiums. It indicates how deeply insurance is embedded in the national economy.

• Insurance Density: The average amount spent on insurance premiums per capita (per person).

Why Pure Protection Matters More Than Ever

Several economic, regulatory, and demographic shifts are converging, making a standalone protection strategy essential for every Indian household.

A. The Reality of Healthcare Inflation

Medical inflation in India is rising at an estimated 10% to 14% annually, significantly outpacing general retail inflation. Advanced clinical treatments, specialized surgeries, and long-term critical illness management can easily cost upwards of 5 Lakh to 10 Lakh. Without a dedicated retail health insurance policy, healthcare costs remain the single largest driver of households slipping back into financial vulnerability.

B. The Fallacy of Mix-and-Match “Investment” Policies For decades, the indian market favored traditional endowment and money-back plans that combined life insurance with savings. However, these financial vehicles often yield low single-digit returns while offering completely inadequate life coverages. Modern financial planning dictates a strict separation:

• For Protection: Pure Term Insurance policies that provide high sums assured (e.g., 1 Crore or more) at incredibly low, affordable premiums.

• For Wealth Creation: Directing surplus funds into high-yielding, regulated vehicles like mutual funds, PPF, or the National Pension System (NPS).

C. Regulatory Push and Greater Affordability

The government and the IRDAl are actively pushing toward the ambitious vision of “Insurance for All”. Key structural reforms, such as the Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Act and strategic exemptions on certain individual policies, are directly aimed at driving down premium costs, simplifying claims processing, and enhancing policyholder trust across both tier-1 and rural markets.

Building Your Personal Protection Framework

A complete safety net cannot rely on a single policy. A bulletproof financial defense framework typically requires a combination of three pillars:

1. Pure Term Insurance: Aim for a sum assured that is at least 10 to 15 times your annual income. This ensures your family can pay off outstanding liabilities (like home loans) and of sustain their standard of living in your absence.

2. Health Insurance with a Super Top-Up: Relying solely on a base corporate plan is risky. Secure a personal family floater plan and attach a Super Top-Up plan to exponentially increase your overall sum insured at a fraction of the cost.

3. Personal Accident & Critical IlIness Riders: Health insurance covers hospital bills, but a critical illness or permanent disability disrupts your regular earning capacity. These riders provide lump-sum payouts upon diagnosis to keep your household running smoothly.