India’s Insurance Market: IRDAI Eyes Landmark Commission Overhaul to Rein in Mis-selling

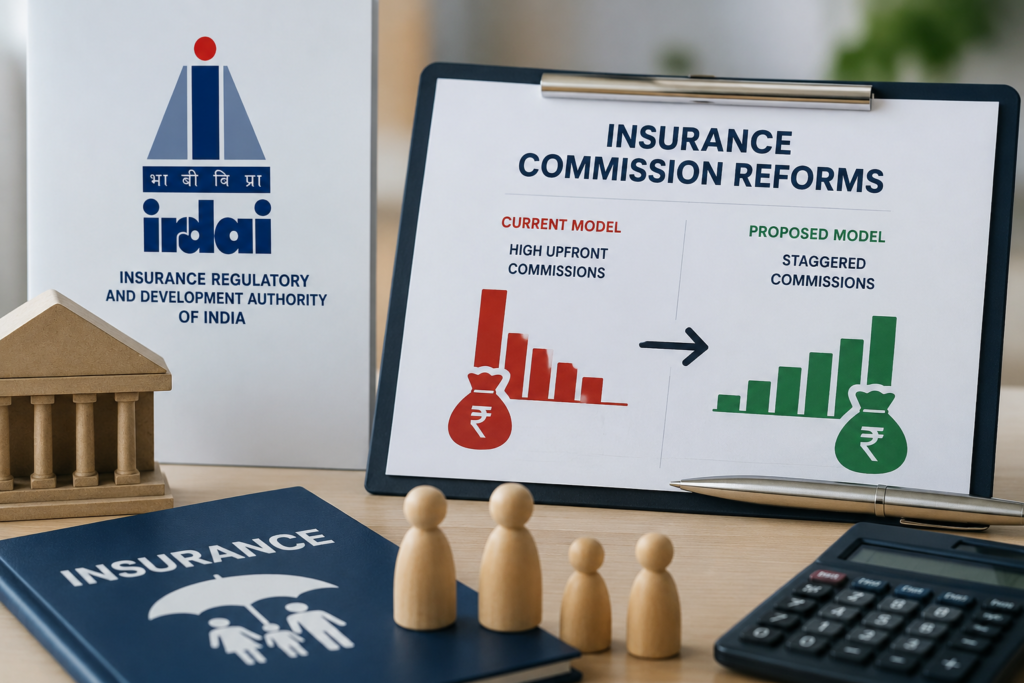

India’s insurance regulator is planning one of the biggest changes to insurance distribution in years, proposing a shift from hefty upfront commissions to a staggered payout model aimed at reducing mis-selling, improving customer retention and aligning the industry’s incentives with long-term policyholder interests.

India's insurance regulator is considering a major overhaul of commission structures to discourage mis-selling and strengthen long-term customer outcomes across the insurance industry.

IRDAI Set to Redraw Insurance Commissions in Push to Curb Mis-selling

NEW DELHI: India’s insurance industry could be on the cusp of one of its most significant regulatory overhauls in recent years, as the Insurance Regulatory and Development Authority of India (IRDAI) considers sweeping changes to the way insurance distributors and agents are compensated.

The proposed reforms, first reported by Reuters, seek to replace the long-standing practice of large upfront commissions with a staggered commission structure spread across the life of an insurance policy. The move is aimed at addressing concerns over mis-selling, improving policy persistency and encouraging distributors to focus on long-term customer relationships rather than one-time sales.

If implemented, the reforms would fundamentally reshape the economics of insurance distribution in India, affecting insurers, agents, brokers, corporate intermediaries and digital insurance platforms alike.

The current commission structure has long been a subject of debate within the industry. In several insurance products, particularly life insurance, distributors can receive a substantial portion of their total commission in the first year of a policy. Critics argue that this model encourages aggressive selling practices, where products may be recommended primarily because they offer higher commissions instead of being the most suitable option for customers.

Industry experts have also pointed to high policy lapse rates as evidence that customers are often sold products that do not match their financial needs or long-term objectives. When policies are discontinued after just a few years, policyholders lose value while insurers incur significant acquisition costs.

The regulator’s proposed changes seek to address these structural issues by aligning distributor earnings with the duration of a policy. Instead of receiving a large payment immediately after a sale, distributors would earn commissions over several years, encouraging them to provide ongoing service and maintain customer engagement throughout the policy term.

Such a model is already common across several mature insurance markets, where regulators have increasingly focused on customer outcomes, transparency and responsible selling practices.

The proposed reforms are expected to form part of IRDAI’s broader effort to strengthen governance and improve consumer protection in the insurance sector. Over the past few years, the regulator has introduced several initiatives aimed at making insurance products simpler, improving claim settlement standards and enhancing transparency across distribution channels.

The latest proposal reflects a growing regulatory emphasis on ensuring that insurance remains a long-term financial protection tool rather than a product driven by sales incentives.

For insurers, however, the transition could require significant adjustments.

Companies may need to redesign compensation structures, modify distribution agreements and recalibrate business strategies that have historically relied on upfront commission payments to drive new business. While the reforms could temporarily slow new policy sales in certain segments, analysts believe they could ultimately improve customer retention and reduce policy lapses, creating healthier economics over the long term.

Insurance agents and intermediaries are also likely to face a changing business environment. Those who depend heavily on upfront commissions may see initial earnings decline under a staggered payout system. At the same time, advisers focused on long-term customer servicing could benefit from more stable and recurring income streams.

Digital insurance platforms and technology-driven distributors may be relatively well positioned if the reforms encourage advisory-led sales and stronger customer engagement throughout the policy lifecycle.

The proposals come at a time when India’s insurance sector is undergoing rapid transformation. The government has announced plans to permit 100% foreign direct investment in insurance, while the regulator continues to push towards its ambitious vision of “Insurance for All by 2047.”

At the same time, insurers are navigating rising healthcare costs, increasing climate-related risks, evolving consumer expectations and accelerating digital adoption. Against this backdrop, improving trust in insurance distribution has become a central policy objective.

While IRDAI has not yet released a formal consultation paper, industry participants expect detailed proposals to be circulated in the coming weeks before any final framework is notified. As with previous regulatory reforms, stakeholders across the insurance ecosystem are expected to provide feedback before the new rules are finalised.

If adopted, the commission overhaul would mark one of the most consequential reforms to India’s insurance distribution landscape in years. Beyond changing how distributors are paid, it would represent a broader shift towards rewarding advice, customer service and long-term policy ownership over one-time product sales.

For policyholders, the reforms could translate into better advice, greater transparency and stronger alignment between distributor incentives and customer interests. For the industry, they signal a regulatory push toward sustainable growth built on trust rather than transaction volumes.

As India’s insurance market continues to expand, the success of these reforms may ultimately be measured not only by how commissions are paid, but by whether they help create a more customer-centric insurance ecosystem capable of supporting the country’s long-term protection needs.